Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv Your Bottom Line CNN December 29, 2012 6:30am-7:00am PST

6:30 am

flight had taken off from the czech republic. we want to update you now of the investigation into two firefighters ambushed battles the fire in upstate new york on christmas eve. police arrested the neighbor. dawn nguyen. she bought a rifle and shotgun for suspect william spengler who later killed himself. nguyen faces federal charges she lied to authorities. spengler couldn't buy the guns legally because he was a convicted felon. he had them with him during the attack. thanks for watching. see you at the top of the hour. it's been fun. >> so good to have you here in atlanta. a happy new year to all of you out there. your bottom line starts right now, and then as she said, alison will be back with you the next couple of hours. go make some good memories.

6:31 am

thanks. see you at the top of the hour. govern, everyone. i'm christine romans, welcome to our help desk special. the best way to make money is make sure your money is working for you. be honest. maybe you'd rather go to the dentist than get an annual checkup of your money. here goes. sit down. it won't hurt. you won't have the to give up your morning latte or anything like that. three drivers for your health, job, investment and health. a great year for the s&p 500. did you miss it? the s&p is up around 13% so far this year. the dow is above 13,000 again. calm it the ben bernanke rally. his fed pumping billions of dollars into the company, and stocks are loving it. but individual investors have missed it. stock, mutual fund outflows upwards of a trillion dollars so far this year. don't feel bad. hedge funds running scared, too. what's been scaring everybody? the fiscal cliff, anemic u.s. growth, europe's financial crisis, china's slowdown.

6:32 am

so proceed, but proceed with caution. co-founder and president of ulta capital management, jack otter, editor and author of "worth it, not worth it" and walter upgrade, editor for cnn. figure how much money in stocks, how much in bonds largely determined how for a until you retire. the faurter you go the more in stocks. then stick to it. don't get swayed by gloom or euphoria. this year, per effect example. people scared, didn't invest much in stocks and a good year. s&p up about 16% year to date. bonds rose. diversified portfolio 4%. can't outguess them. don't try. >> make a strategy and stick with it. many viewers may be in the same spot. what one investor is worried

6:33 am

about. lyn. >> i should have been very aggressive, but i played very conservative, and so how do you play catch-up? >> what's the best catch-up strategy? >> that is a very dangerous question. it's a very common question, and understandable, but the problem is, we all tend to make our decisions based on whatever has just happened. so this woman probably got scared in the financial crisis. her stocks plummeted and then she sold them and went conservative. now, of course, stocks doubled since march of '09 at the bomb um. now thinking, maybe it's time to get back in stocks. you pointed, people have been selling mutual fund. they will start buying and what will probably happen, they'll go down again. break the cycle. stick to the plan walter said. good default beginning would be 60% stocks, 40% bonds. 's in my book i laid out four mutual funds to get that diversified mix. maybe a little more aggressive. 70-30, maybe 50-50 if you're conservative. the point, stick with it. don't change it because what

6:34 am

just happened in the market, you'll always get many slaed that way. >> one tried and true way to actually get your balances up in your retirement. putting more money in. if you're playing catch-up, no the just about the strategy you outline. excellent one, but putting more money in to play catch-up to add money and time to the right balance of risk and stick with the plan. >> and time is your best friend. younger americans also care about retirement, and they've got more time working on their side. here's a good question we've been asked many times. >> my question is, regarding a 401(k), i have one going but a.m. not sure what mire target percentage i should be contributing to that. i'm 30 years old now. to retire comfortably, eventually, what should i be trying to put away? >> hmm. a good question. he's 30. he's got a good 25 or, at least 25 years of investing. fidelity says the end goal, eight times your last year's salary. some financial planners say 10 to 12 times if you're a high

6:35 am

earner. carmen says, try to come up with a flub. nice to have a number goal. at 30, how do you know where you'll be or what you'll be doing the next 30 years? here's what you put away. at least if you can allot 10%. right? especially if there's a company match. the trick, actually put stuff away. no hedging or hemming or hawing, put the stuff in there especially at 30. time is on your side. if he waits another couple years with compound interest he'll lose multiple amounts of money. put away 10%, if you can put away more, you can adjust. think outside the 401(k). young, ax to a roth as well. put more money in there. >> we have very easy calculator on the website, and that is -- >> walter makes it so easy. cnnmoney.com. makes it so easy, you have no excuse, people. >> go there'sput in your age, how much money you make, how much you saved and a recommendation of what percentage of your salary you should save this year.

6:36 am

carmen's right. at least 10%. probably try and get it up to 15%. >> 15, too? >> absolutely. so many unknowns. give to the max. this guy, he's young. probably doesn't have a family yet. and so he doesn't believe me, but when he's 40 and has two children he's going to say, darn, i wish i put that extra money i spent on i don't know what into my 401(k). >> absolutely. >> we start about having kids. putting away for the 529, blah, blah, blah. retirement always comes first. thanks for joining us, walter, carmen and jack, stick around. if you want the calculator to work for you, visit cnn money.com. all the latest news on the economy, business, stock market. is there a recovery happening in your neighborhood? um canning up, we'll show you where the hottest housing markets are, and we're going to get you smart on renting, buying and refinancing. at a dry cleaner, we replaced people with a machine.

6:37 am

what? customers didn't like it. so why do banks do it? hello? hello?! if your bank doesn't let you talk to a real person 24/7, you need an ally. hello? ally bank. your money needs an ally. make a wish! i wish we could lie here forever. i wish this test drive was over, so we could head back to the dealership. [ male announcer ] it's practically yours. test drive! but we still need your signature. volkswagen sign then drive is back. and it's never been easier to get a jetta. that's the power of german engineering. get $0 down, $0 due at signing, $0 deposit, and $0 first month's payment on any new volkswagen. visit vwdealer.com today.

6:38 am

[ buzzing ] bye dad. drive safe. k. love you. [ chirping, buzzing continues ] [ horn honks ] [ buzzing continues ] [ male announcer ] the sprint drive first app. blocks and replies to texts while you drive. we can live without the &. visit sprint.com/drive. i need you.

6:39 am

i feel so alone. but you're not alone. i knew you'd come. like i could stay away. you know i can't do this without you. you'll never have to. you're always there for me. shh! i'll get you a rental car. i could also use an umbrella. fall in love with progressive's claims service. finely here. look at the biggest gains in home prices. demand is coming back. from september, check out phoenix. 20% higher than the year before. home prices up 20% year over

6:40 am

year in phoenix. detroit, up 7.6%. look at miami. up 7.4%. those areas were slammed by the housing crisis. now they're making solid improvements, but you know the old saying, all real estate is local. prices in new york and chicago in september dropped from the year earlier. obviously, we have a really long way to go, but the price plunge coupled with super cheap mortgage rates make houses affordable for the first time in years. 30-year fixed rate mortgages covering around 3.3% now. fixed year, 15-year fix around 2.6%. that's according to freddie ma'am. people who financed a little over a year can ago, are going back wondering if it's time to do it again. underwater, less than 720 credit score or no down payment are wondering how long the rates will stay low and whether these affordable prices will last. carmen and jack are back with me and with zillo.com, a real

6:41 am

estate website based in seattle. paul from california send an e-mail, "i have enough money in my emergency fund right now to put a down tamt on a house with interest rates where they are does it make any sense to buy or to stay renting" what do you think paul should do? >> he shouldn't deplete his emergency fund. the good news, while home values are increasing in a lot of places, in most places they're only increasing by 2% or 3% over the next year, what economists are predicting. places like phoenix are the outlayer right now. he has time with the low prices. we also expect really low mortgage rates to stick around for at least the next year. so you've got to have an emergency fund, because if somebody loses a job, if something changes in your financial situation, buying a home is a big commitment, and you've got to be able to continue paying that mortgage. so have your emergency fund, but also have your down payment ready, and when you have your emergency fund together, that's the time to make the down payment. don't mix the two. >> listen to this dilemma, also

6:42 am

weren't i think americans struggle with. >> my husband and i are still paying off a home loan, and we've got some credit card debt. the credit card debt is higher. is it best to pay more on the house or to get rid of the credit card debt first? >> i know what carmen is going to say. >> listen, now -- well, you know, you just talked about mortgage rates. right? how low they are. this is incredibly cheap money, and also, she lives in a place where the housing market is actually going up. it's even cheaper. probably zero. she needs to pay off those cards. put more money towards those cards every single month, and just get that out of the way. they probably have really high interest rates compared to your mortgage and there's no intrinsic value what you bought with your credit card. your home is actually an asset, it has value. it's not the same kind of debt. you can't mix up the two different kinds of loans. >> a lot of first-time home buyers are saying they're not able to grasp this yet.

6:43 am

no money for a down payment or the credit score isn't good. do you think rates will stay low enough long enough that people have time to repair their personal balance sheets and then, and then move? >> well, you know, the fed says into late 2014, early 2015, but also peggedful to the unemployment rates. should the unemployment rate improve quickly we might see rates move higher. i hate to mix these two up, because the problem is, yes, we all want to seize these great rates, but if you're not ready, you could dig an even deeper hole by not preparing your personal balance sheet, jumping into a house you can't afford and the potential problems there are much worse than, yeah, having to settle for the 5.4% mortgage. >> let me ask amy about the whole rent versus buy thought. in places like here in new york city. listen. >> how in the world do you save for a house? >> how in the world do you save for a house? i'm going to ask amy and jack

6:44 am

this. how much do you need to have a down payment for a house at this point? >> well, the good rule of thumb today is 20%, and you also have to have really good credit to be able to get some of these really low mortgage rates. so put the money aside over time, but, you know, as paul mentioned before, when you buy a house is your own personal financial situation. you have to be ready for that, and don't jump into it now because of these low prices and low mortgage rates. if you're simply not ready. it has to be the right time for you, and as we learned over the last decade, really bad things can happen when people jump into this too early. >> jack, what's the saving plan people need to have for putting the money aside? >> number one, how much will it cost you? look around when you plan to live and realize i freed to raise $25,000 for a down payment. two things. one, it's realistic. not going to do that by tomorrow. number two, you can have that very specific goal and do the math and know, i can do it in two years.

6:45 am

that's $1,000 a month. is that even possible? if so, act like congress. raise revenues and reduce spending. so this is what we're going to cut out of our budget, and this is how i'm going to take that extra part-time job or whatever it takes to make that money. >> amy, how do you characterize the market right now? it's in recovery but nowhere near where it was in 2007 and 2008? >> that's right. it really varies by market, in most places across the u.s., the housing market bottomed, but this is a long and slow slog to recovery. our economists predict over the next year across nationwide, home values are only going to rise about 2.5%. it is going to take years and years for us to get back where home values were in most places at the peak. for people thinking about buying, you do have some time to take advantage of these low prices. >> all right. and i know we've been -- wow. profiled people who were financed a couple of times, looking at it again with low mortgage rates. thanks. and most homes and investments are made possible by

6:46 am

paychecks. up next, the smartest moves you can make to get a job or get a better one right now. we asked total strangers to watch it for us. thank you so much. i appreciate it. i'll be right back. they didn't take a dime. how much in fees does your bank take to watch your money? if your bank takes more money than a stranger, you need an ally. ally bank. your money needs an ally. campbell's has 24 new soups that will make it drop over, and over again. ♪ from jammin' jerk chicken, to creamy gouda bisque. see what's new from campbell's. it's amazing what soup can do. gives you 1% cash back on all purchases, plus a 50% annual bonus. and everyone...but her likes 50% more cash. but i'm upping my game. do you want a candy cane? yes! do you want the puppy? yes!

6:47 am

do you want a tricycle? yes! do you want 50 percent more cash? no! ♪ festive. [ male announcer ] the capital one cash rewards card gives you 1% cash back on every purchase plus a 50% annual bonus on the cash you earn. it's the card for people who like more cash. what's in your wallet?

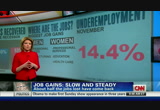

6:49 am

oh. the jobs market. it remains the biggest problem in the american economy. three years after the recession ended the jobless rate stands it's a 7.7%. we've made progress. men have gained back half of all the jobs lost during the great recession. women doing a little better. they've gained back 53% of the jobs lost. where are the jobs? for men the biggest gains in professional services. factory, long-lasting goods like cars and retail. women also made big gains in professional services. education, health care have also hired a lot of women. but many of the jobs coming back are lower paying than the jobs lost, and we look at this thing also called the real unemployment rate, underemployment. his 14.4% in november according to the government including unemployed, working part-time who want a full-time gig and

6:50 am

other satached to the workforce. here for advice, carolyn, long-term or under employed, how can they brand themselves for a fire hiring boom in the next few years? >> have a story apart from job search. employers want to see you're busy, staying active and current, still in and around companies and other people. you want activity, whether it's projects or research you're doing. >> fill the gap on the resume with peoples names who you meet. >> stay in the professional groups. remember, mine orpty, women's group, even if you don't have a job you'refantastic way to network. >> and find a nonprofit that can use whatever skill it is you want to be using in the private work force. whether it's planning parties or being their accountant or

6:51 am

building a new web page or designing offices, you go to the job interview and say, yeah, here's the web page that i designed. you've got a lot on your resume instead of i'm home sending out resumes. >> we met alicia amp she's been out of work since april. listen to what her big concern is now. >> we need help. i believe that they should extend it -- >> unemployment benefits? >> yes. definitely. give us more time to find jobs. >> more time. she thinks things are going to get better next year. she think there's a job that is around the corner for her. she just needs a little more time. how does she make herself appearality an interview that i'm not long-term noed, i'm ready to hire and work now? >> again, part of it is staying busy. like jam and cameck and carmen . second, be aware of what's going on with the company. if she knows what business they're in, it will make the employer feel like she can hit

6:52 am

the ground running and hasn't been out for a long time. >> i think people spend a lot of time looking for a job but it's not necessarily well-targeted time. they say i've been having ads, looking at monster -- but you need a name of someone who can get you in the door. >> we know the stats. the stats are that most people get jobs through people that they know. you've got to stop just applying like jack mentioned, stop sitting at the computer, go out, shake hands, talk to people, don't be shy about letting everyone in your circle know, your facebook friends, everybody, hi, i'm looking for this position, tell your cousins, aunts, uncles, they'll get you the job, not competing against hundreds of resumes and a computer that's sorting you. >> the best possible reference is a former boss or even a former colleague who has seen you do good work and can get your resume to the right person and say, yeah, she used to work here, and she's awesome. >> another concern, thousands of college students looking to get their foot in the door. here's one of them. >> i'm wondering how i'm going to afford a minimum wage job

6:53 am

with all the student loans i have to pay for and just graduated college. >> i wonder about what you think if someone who graduated college should take the minimum wage job and not spend more time looking for a job that might be the first step on a career ladder. what do you advise? >> i don't think it's an either/or thing. i know people who have taken a major low-paying job and then they still keep active looking more long term. >> right. not mutually exclusive. >> that gives you the sense in the interview, look, i'm pouring coffee at starbucks, but i'm doing x and y on the side. the unemployment rate for college graduates is about 4.1% now. so it's actually not awful. ain't great, but it's better than people without degrees. >> those are college graduates who have been in the labor market. if you graduated last may and have never had a job, you're not counted still. >> and don't forget, she mentioned student loansment part of her question was, okay, what am i going, do i'm making minimum wage. she has to make sure she knows what kind of loan she has. go and see, do i have a federal loan, a private loan? can i file for income-based

6:54 am

repayment. so if she has a minimum wage she's not going to get a student loan bill for $500. she's got to match what she makes with her student loan payments and be proactive. even if you're not working. >> is the labor market going to be better for the class of 2013 you think? >> we hope. >> i think so. >> i think it will. i really do. a little better. >> carmen's point is crucial. you can get your student loan payment as low as 10% of your discretionary income. >> yeah. >> if it's a federal loan. >> yep. income-based repayment. >> exactly. >> income-based repayment. google it, folks. thank you. nice to see you today. for many students, education loans have become a de facto mortgage, taking decades to pay off. coming up, how to make sure your kid isn't saddled with loans for years to come. the capital one cash rewards card

6:55 am

gives you 1% cash back on all purchases, plus a 50% annual bonus. and everyone likes 50% more... [ midwestern/chicago accent ] cheddar! yeah! 50 percent more [yodeling] yodel-ay-ee-oo. 50% more flash. [ southern accent ] 50 percent more taters. that's where tots come from. [ male announcer ] the capital one cash rewards card gives you 1% cash back on every purchase plus a 50% annual bonus on the cash you earn. it's the card for people who like more cash. 50% more spy stuff. what's in your wallet? this car is too small.

6:57 am

so many parents, i know you're worried about your children graduating from college with a mountain of debt. and you've got a right to be. student loan debt has exploded. it's now bigger than credit card or auto loan debt. now there are smart ways to keep the borrowing down in the first

6:58 am

place. you don't want to let that mountain grow over time. you want to keep it as small as possible in the first place. here's how one grad did it. at 24, greta russler has her bachel bachelor's degree. figuring out how to pay for it wasn't easy. >> i only applied to two schools, both in state, because those were the only ones that were really going to be a reality. >> she chose georgia state university where a four-year degree cost just over $21,000. she earned a scholarship to cover tuition, loans and a part-time job paid for living expenses and study abroad. >> i ate a lot more ramen than i am proud to admit. i had a mattress on my bedroom floor. my clothes were kept in boxes on a bookshelf in my closet. i was living the college life. >> russler graduated last year with $7,000 in loans, well below the average in of nearly $24,000. she did all the right things. you have to keep the debt down

6:59 am

in the first place. scour for grants and scholarships. remember, it's cheaper to save for college than to borrow. that $25,000 loan will likely set you back $35,000 with interest later. and get a head start earning college credit so you can graduate in three years. make sure the school you want to attend will accept those credits. >> a.p. classes, advanced standing exams, these are all great ways of getting college credit while you're still in high school. >> financial aid expert mark cantowitz says don't borrow more than you can pay. >> your total debt at graduation should be less than your annual starting salary. >> now some colleges are trying to make education more accessible. belmont abby in north carolina lowered tuition by 33%, and florida's governor is pushing community colleges to offer a $10,000 bachelor's degree. >> i believe that we absolutely will accept a governor's challenge and develop one or more bachelor's degrees that

185 Views

1 Favorite

Uploaded by TV Archive on